Elder financial abuse happens when someone takes advantage of an older person’s trust, vulnerability, dependency, or financial authority to access or control their money, investments, insurance policies, or property. It may involve a family member, caregiver, power of attorney, advisor, or another trusted person. If funds were moved, investments were changed, beneficiaries were altered, or financial decisions were made under pressure or without proper understanding, the situation may deserve legal review.

Elder financial abuse happens when someone takes advantage of an older person’s trust, vulnerability, dependency, isolation, or declining capacity to gain access to their money, investments, insurance products, property, or financial decisions.

This abuse can come from many directions. It may involve a family member, caregiver, friend, attorney under a power of attorney, financial advisor, investment representative, insurance advisor, or another trusted person.

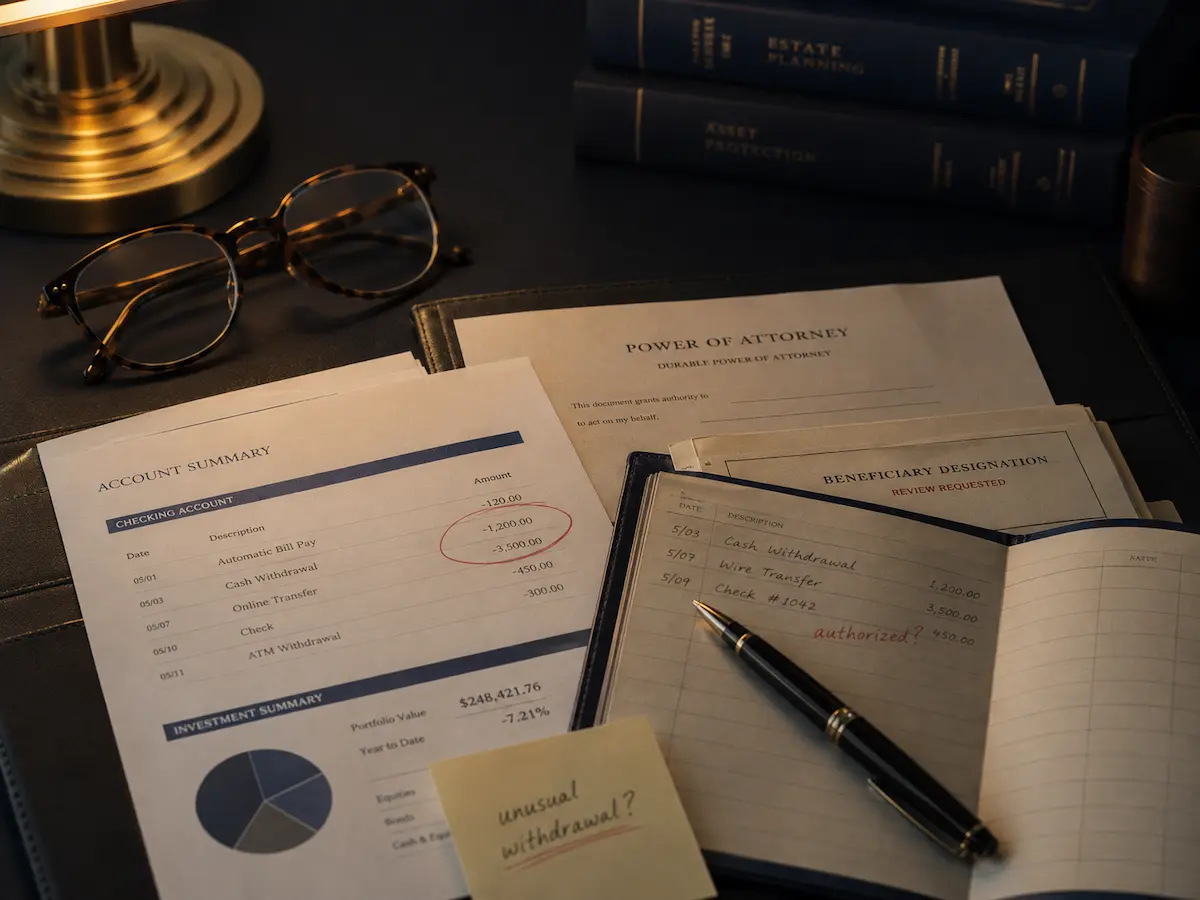

In some cases, the abuse is obvious: money disappears, accounts are drained, signatures are forged, or investments are changed without proper consent. In other cases, the situation is more subtle. An older person may be pressured into changing beneficiaries, moving investments, signing documents they do not understand, lending money they cannot afford to lose, or giving someone control over their finances.

Financial abuse is especially serious because many older investors do not have time to recover from major losses. A lifetime of savings can be damaged quickly, and the emotional toll can be just as harmful as the financial one.

Not every poor financial decision is elder abuse. But when someone exploits trust, pressure, confusion, dependency, or authority to benefit themselves at the expense of an older person, legal action may be possible.

Elder financial abuse can take many forms. Sometimes it involves outright theft. Other times, it involves manipulation, pressure, or misuse of authority.

Common examples include:

In many cases, elder financial abuse is not a single event. It is a pattern that grows over time.

Elder financial abuse is often hidden behind a relationship of trust.

The person causing harm may be someone the older adult depends on for transportation, banking help, caregiving, family support, or financial guidance. That makes it difficult for the older person to speak up, especially if they feel embarrassed, confused, afraid, or loyal to the person involved.

Family members may notice something feels wrong before they can prove it.

Some warning signs include:

These signs do not automatically prove abuse. But they do warrant a closer look.

When an older investor works with a financial advisor, investment dealer, insurance advisor, or portfolio manager, that professional is expected to understand the client’s situation and make appropriate recommendations.

This becomes especially important when the client is elderly, retired, widowed, isolated, dependent on investment income, or experiencing health or cognitive changes.

A financial professional should not ignore warning signs. They should not recommend strategies that are clearly inappropriate for the client’s age, needs, risk tolerance, or ability to recover from loss. They should not allow suspicious transactions to proceed without proper review.

When financial professionals fail to act carefully, fail to recognize vulnerability, or participate in harmful recommendations, they may contribute to the loss.

A strong elder financial abuse claim usually depends on showing what happened, who benefited, what the older person understood, and whether proper consent was given.

Helpful evidence may include:

A case may be stronger when the records show a clear change in financial behaviour, unexplained movement of funds, pressure from another person, unsuitable recommendations, or decisions that did not match the older person’s long-standing wishes or financial needs.

For example, if a retired investor who needed safety and income was moved into high-risk or illiquid investments, that may support a claim. If a trusted person used a power of attorney to move money for their own benefit, that may raise serious legal concerns. If beneficiary forms were changed when the person lacked capacity or was under pressure, that may need to be challenged.

If you suspect elder financial abuse, it is important to act carefully and quickly.

Start by gathering records. Do not rely only on verbal explanations from the person who may have benefited from the transaction. Documents often tell a clearer story than memory alone.

It can help to write down a timeline:

If the older person is still able to participate, their own recollection may be important. If capacity is an issue, the timing of decisions may become especially relevant.

You do not need to prove everything before speaking with a lawyer. The first step is understanding whether the financial activity should be reviewed and whether legal action may be available.

If you believe an older investor has been financially exploited, pressured, misled, or placed into unsuitable investments, Geller Law can help you understand the available options.

Harold Geller has worked with clients in claims involving elder financial abuse, investment losses, advisor misconduct, unsuitable advice, insurance disputes, and financial negligence.

A consultation can help determine whether the loss was caused by improper conduct, whether a financial advisor, dealer, insurer, or trusted person may be responsible, and what steps can be taken next.

Click here to request a free consultation to discuss a potential elder financial abuse claim.